“Compound interest is like a snowball rolling down a hill. The real trick is to start the snowball on top of the hill.” – Charlie Munger.

Compounding is a fascinating phenomenon. You’ve probably heard of a problem being compounded and getting worse. But it can improve your life incredibly if something positive is compounded.

In the financial world, compounding is usually about building wealth. The recipe includes some common ingredients: how much you save, a positive rate of return on your investments, and time. I believe that time is the most crucial ingredient for compounding. But before I explain why, let’s take a moment to consider the thing people usually focus on – the rate of return.

For example, let’s start with 7 percent. Whether it’s on financial media or YouTube videos, I’ve seen enough to suggest that many people don’t think a 7 percent annualized rate of return is that impressive. It almost seems like that’s something anyone could achieve just by showing up as an investor.

Yet earning a 7 percent return over time is more of an accomplishment than you might think. For starters, human behavior, influenced by emotional factors like greed or fear, can hinder progress. It has always been, and it always will be, that way for some. But let’s hope not for you.

But let’s say you’ve tamed your emotions. Even if you were a robot that behaves rationally, it doesn’t mean you’re out of the woods. For example, look at the history of the US stock market. There have been times when you could have invested passively for 20 years and still not seen a 7 percent return. Of course, most periods have resulted in higher returns. The main point is that a 7 percent return shouldn’t be dismissed lightly.

Let me clarify two things.

- There’s a number out there for you—a certain rate of return needed to reach your financial goals. But how high does it have to be? If you say, “as high as possible,” that’s understandable. I’d like the same, but I also try to be mindful of the risks involved in reaching those returns.

- A 7 percent return alone is somewhat arbitrary and even meaningless if inflation isn’t considered at the same time. That’s because our actual returns after inflation are what build real wealth. Recent history has shown inflation, as measured by the CPI, to be around 3 percent or less. So, a 7 percent return would translate into roughly a 4 percent real return. If future inflation turns out to be significantly higher than 3 percent, a higher portfolio return would be necessary to maintain the same purchasing power.

With these caveats, let’s return to the topic of compounding. While getting a good rate of return is important, it’s not the only factor to consider. Let’s visualize how powerful compounding can be and then explore what I call the “Die with Zero” dilemma.

Visualizing the Power of Compounding

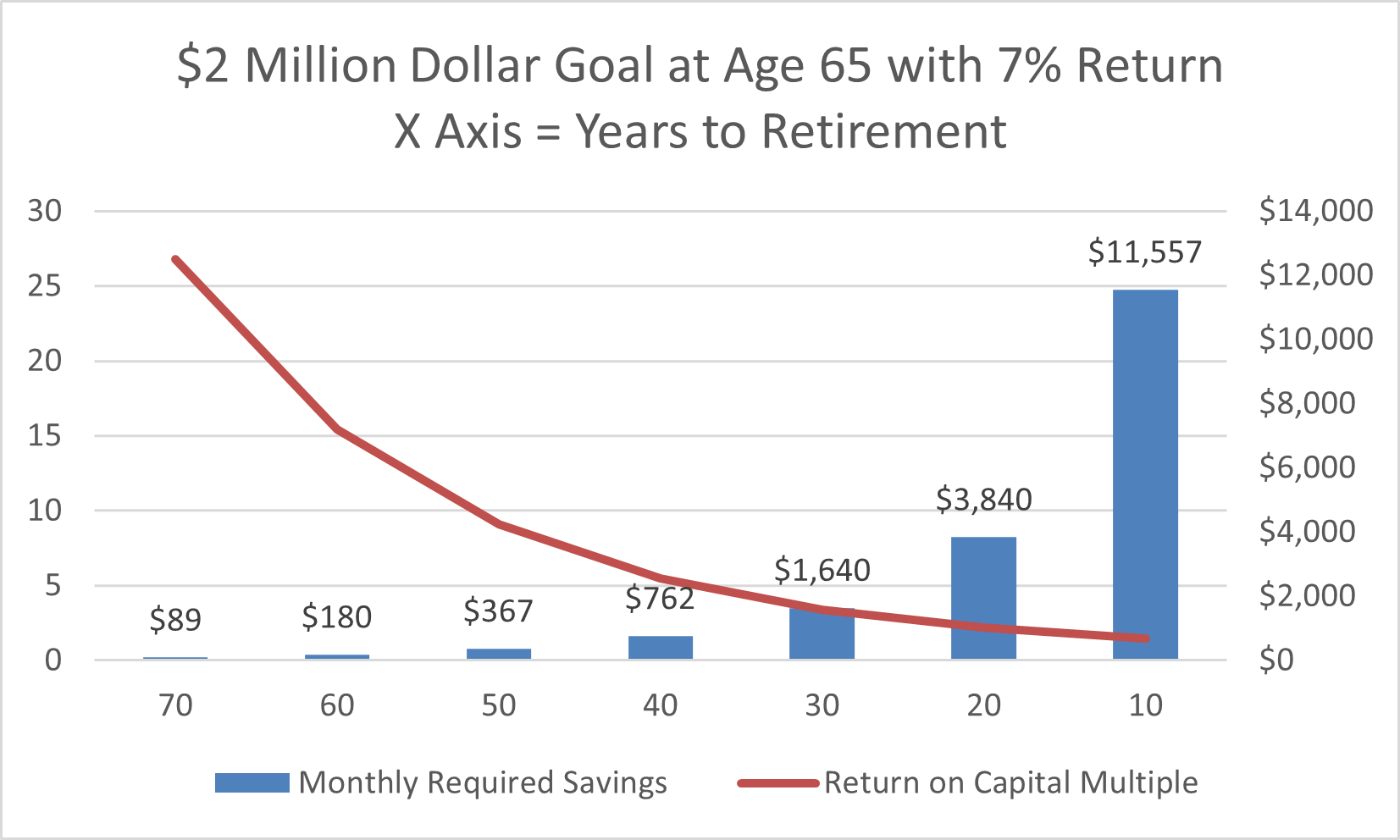

There are many ways to demonstrate the power of compounding. But today, let’s examine it through a simple retirement example with a twist. Suppose your goal is to build an investment portfolio worth $2 million by your target retirement age of 65. We’ll also imagine that today is your 65th birthday! At a 4.5% initial withdrawal rate (with several other assumptions), we’ll assume this can provide roughly $90,000 of inflation-adjusted income for the rest of your life, supplementing Social Security.

Continuing with this example, as fate would have it, no matter how long you saved in the past, you could only achieve a 7 percent annualized return (after fees and expenses), and you always started your investment journey with a portfolio of $0. How much would you have needed to save each month to reach your goal today? The chart below may help visualize the answers.

The chart shows that if you’re 10 years away from retirement (age 55) and start your savings habit then, you’d need to save $11,557 per month. If you are 40 years away from retirement (age 25), you’d need to save $762 per month. If you were lucky enough to have a parent start saving for you 5 years before you were born, they (and you) would only need to save $89 per month. In that letter case, you would also achieve approximately a 27-times return on capital, as indicated by the red line.

This chart doesn’t even tell the whole story about compounding. If a trust had been established on your behalf 130 years before your retirement, the trustees (and eventually you) would need to save about $1.34 each month to reach your $2 million goal today. That’s right; it’s just over a dollar per month. This means that saving less than $2,100 in total could grow into a portfolio worth $2 million—almost a thousand times the initial capital with just a 7% return.

Shall we continue with the absurdity? Investing one cent ($0.01) per month for 200 years (a total of $2) results in a $2 million portfolio. Okay, I’ll stop here. The point is that compounding can be mind-blowing over long-term horizons. Time makes the results seem magical.

The “Die with Zero” Dilemma

While time might be the key ingredient in compounding, a lack of time (whether perceived or real) can be quite an obstacle. And as mortal beings, none of us individually has a 130 or 200-year investment horizon!

You probably want to make the most of life with the limited time you have. That means living in the moment, enjoying the now, and making memories while you still have the health to do so. Money can play a significant role in all of that.

In fact, that’s one of the central arguments in Bill Perkins’ book, Die With Zero. Perkins offers compelling reasons to spend more money at the appropriate times in your life. In one of his stories, the main message was to save less in your 20s, since it’s the time when you usually have the most health and energy. You’re also typically not tied down by family and can have more adventures.

However, one of the financial reasons Perkins supported this age-based spending approach was that you’re more likely to earn a higher inflation-adjusted income as you get older, with peak earnings typically occurring in your 50s or 60s.

This entire line of thinking makes sense and is emotionally compelling as well. However, we should recognize that this approach competes with the mathematics of compounding shown earlier. That’s because compounding is a non-linear process. Instead of a straight-line projection, you get exponential results. The type of leverage you gain from saving at an earlier age is harder to compensate for later in life.

If you appreciate the compounding effect, you’ll have stronger motivation to start saving as early as possible; however, here’s another challenge. Imagine you’re already in your 50s and have reached what you believe is your peak earning period. If you’re behind on your retirement goals, it may require an unexpectedly large portion of your savings to catch up. Alternatively, you might seek higher returns on your investments, but that involves additional risks and considerations.

What further complicates this is what I observe with my own clients in this age group. This stage of life is when the desire for work and spending optionality seems to be at its highest! Many people want to spend less time at work and more time with their families, as well as pursue other activities that bring meaning and purpose.

Most of my working-age clients are in the technology industry. Although job markets are always unstable, the tech sector feels notably different now due to the rise of Artificial Intelligence. Even if you’re statistically more likely to earn a higher salary in your 50s (recall one of the reasons to spend more when you’re younger), you might not feel comfortable depending on that. Technological change and disruptions are ongoing, and you want to be resilient to that.

Reconciling Two Powerful Forces

I suppose all these musings ultimately lead to a dilemma. Compounding is a powerful force, but our desires and life circumstances can make it challenging to reap the benefits. Is there a solution or way out of this? This tension is what makes financial planning so incredibly interesting to me. There are no easy answers, and the answers that are there will be unique to you. But I’ll leave you with a few things to consider.

Remember that money is not the only source of capital you have. The others are energy, time, and attention. And as writer Carl Richards says, sometimes how we invest those matters more than how we invest money.

But since money is so integrated into our lives, like an underlying current, just embrace the cliché of finding the right balance. It’s about discovering and maintaining a lifestyle that brings joy and well-being, without relying entirely on spending more money. It could involve taking a page from the minimalism movement.

Understanding the power of compounding may give you more motivation to save. But it might not. You need to discover the real reasons to save money. As suggested in the last blog link, it may be more about things like freedom and flexibility.

You might be wired to spend more money now rather than saving for an uncertain future that may never happen. That’s perfectly fine; there’s no judgment here. Just keep in mind that money can bring happiness up to a point. However, its impact lessens over time, and we quickly get used to new lifestyle levels. This phenomenon is often called hedonic adaptation.

Finally, if you are going to get on the metaphorical compounding train, get the right systems and habits in place for saving and investing. Whatever time you have left on the journey, use that. With compounding, we want time to do as much of the heavy lifting as possible.

If you have comments or questions on this piece, please drop me a line at: [email protected]

References

- https://krishnawealth.com/will-the-4-percent-rule-work-for-your-retirement/

- https://www.diewithzerobook.com/welcome

- https://krishnawealth.com/cultivate-your-optionality/

- https://krishnawealth.com/is-a-dose-of-minimalism-the-cure/

- https://krishnawealth.com/the-real-reasons-why-you-should-save-money/

- https://krishnawealth.com/have-goals-but-focus-on-systems/

The information on this site is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Krishna Wealth Planning LLC (referred to as “KWP”) disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.

KWP does not warrant that the information will be free from error. None of the information provided on this website is intended as investment, tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall KWP be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the materials in this site, even if KWP or a KWP authorized representative has been advised of the possibility of such damages.

In no event shall KWP have any liability to you for damages, losses, and causes of action for accessing this site. Information on this website should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.