8-Minute Read

There’s always much to think about when it comes to the markets and the economy. But let’s talk today about something a little more under your control: bank accounts. You might take these for granted, but they are essential to your financial foundation. These might even be the accounts you view every day, as it’s often not the healthiest decision to view your investment accounts daily. But what exactly is so interesting about bank accounts?

I’ve come across many people who do something like this. They have an emergency fund at Bank A, a vacation fund at Bank B, and a new car fund at Bank C. Perhaps on top of that, they have multiple “goal-based” accounts in each of these banks. Does this sound like you?

If so, I doubt you’re doing this because you love extra paperwork or dealing with multiple accounts. You’re probably doing it to create a form of “friction” in your financial matters and to better clarify what dollars are available for what goals.

In many cases, having multiple accounts is a physical solution to a psychological need. But what if financial technology (often called FinTech) can be used to more efficiently solve this problem?

For those of you who’ve worked with me for some time, you’ve probably heard me refer to something called Flourish Cash. We’ll hit on some of their benefits in this piece. We’ll also focus on their new “buckets” feature, which may make the multi-bank strategy obsolete for many.

In this piece, we’ll explore:

- Why Our Brains Love Buckets

- The Hidden Costs of Managing Multiple Banks

- A Solution – Flourish Cash “Buckets”

- How to Move from “Multi-Bank” to “Multi-Bucket”

- Addressing the “Eggs in One Basket” Concern

Psychology of Mental Accounting: Why Our Brains Love Buckets

Much of this discussion centers around “mental accounting”. It’s a concept, pioneered by Richard Thaler back in the late 1990s. It’s the idea that humans treat money differently based on where it came from and what it’s intended to be used for.

Thaler’s research didn’t just look at how we spend money, but where that money came from. He famously identified the ‘House Money Effect’—the tendency to treat windfall gains (like a tax refund, a bonus, or even a $50 bill found on the sidewalk) with less care than our hard-earned salary.

A “where it came from’ example

Imagine you get a $2,000 tax refund. To your brain, this feels like ‘bonus’ money, and you might spend it on a new couch without a second thought. However, if you had to save $2,000 slowly out of your monthly paycheck, you’d likely treat that money with much more reverence. By using Buckets, you can effectively ‘tame’ these windfalls. Instead of letting a refund sit in your checking account where it feels like ‘fun money,’ you can instantly allocate it to your ‘Home Maintenance’ or ‘Emergency’ bucket, mentally transforming it from a windfall into a strategic asset.

An “intended use” example

We also don’t treat all dollars as equal based on the intended use; a “vacation dollar” feels different than an “emergency dollar.” The traditional economic view is that it would be illogical for someone to hold $5,000 in a savings account earning 2 percent while owing that same amount on a credit card charging 20 percent. But people do this because the $5,000 is in their “emergency bucket,” and it’s easier to treat it as off-limits for almost anything, even debt.

There is research to show that simply naming an account (e.g., “Kids’ College”) makes us significantly less likely to “raid” it for impulse buys.

A natural extension of all this is for people to hold multiple bank accounts that are labeled, sometimes literally but not necessarily, for the particular goals they have. It may feel like a necessity, or it’s just a habit that has been ingrained. But for most, it’s just a solution that satisfies a psychological need. But it does come with some costs.

Beyond the Paperwork: The Hidden Costs of Managing Multiple Banks

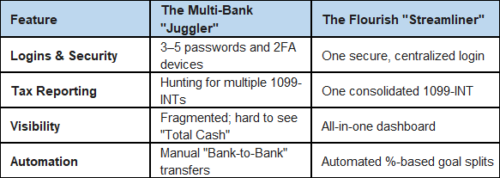

The first cost is not so much financial as administrative friction. When you have multiple banks, think about what you have to keep track of. You have passwords, two-factor authentication, and various personal details that you need to keep up to date across different institutions.

Furthermore, any institution you deal with will send you regular email or physical mail that you must process. And if you have four different banks, you need to deal with four different 1099-INT forms during tax season.

When you’re looking at your net worth at any given time, it can be harder to see your total liquidity at a glance when it’s fragmented. For our clients, that’s not necessarily a huge issue. Our reporting segments cash into its own area of the balance sheet. But one issue we can’t really avoid is the tech behind account aggregation. When it works, it’s great, and you can see real-time values of your accounts. But then the links go stale, and the client needs to come in periodically to refresh them. It’s a mild pain, but an extra task nonetheless.

Finally, the hidden financial costs often come in the form of inertia. Say you have a checking account that’s earning 0.01%. It may be hard to move that money to a different bank earning a higher interest because the “effort” of the transfer feels higher than the interest gain.

A Solution: Flourish Cash “Buckets”

Before we get into this, a brief disclaimer is needed. My firm, as a fee-only firm, doesn’t receive any compensation from Flourish or any third party for recommending their product. I’ve just been happy with how it’s worked for me personally and for many of my clients for years. If any other banking platforms offer a similar service to what I’m about to describe, then I’m all for you using that!

So, how does Flourish Cash work? It’s a way for you to earn a competitive interest rate on your cash without the need to jump from one bank to another. There are no hidden fees or minimum account sizes. Plus, you have full FDIC insurance protection (more on that in the section).

There are few more nuances to using Flourish that I won’t cover in this blog. But you can always refer to their online FAQ page.

But what has intrigued me recently about Flourish is their new “Buckets” feature. You have one account and one login. But you can create an “infinite” number of sub-accounts. They aren’t really accounts per se, in that you don’t have a new account for each. But here’s how it works.

- Custom Labels: You can name your goals. At present, you can create up to 20 buckets (so it’s not really infinite) in any categories of your choice as long as each has a unique name.

- Automated Allocation: You can set percentages (e.g., “Every deposit I make gets split: 50% to General, 30% to Emergency, 20% to Wedding”).

- Easy Editing: It’s a simple process to edit, create, or delete buckets. You can easily move money between buckets and choose which buckets are prioritized when making a distribution.

Back to the mental accounting, it’s like the best of both worlds. You get the mental “permission” to spend from the vacation bucket and the “protection” of the emergency bucket, but with the simplicity of a single statement.

How to Move from “Multi-Bank” to “Multi-Bucket”

If you’ve spent years opening different accounts to keep your goals organized, the thought of consolidating everything might feel like a major project. But the process is simpler than you might think. Here is how you can transition from a “juggler” to a “streamliner” in four steps:

Step 1: Designate Your “Hub”

Simplification doesn’t mean having zero outside accounts. You still need a “financial hub”—usually a traditional checking account—for your day-to-day bill paying, direct deposits, and ATM access. Keep your existing checking account where it is, but view it as the transit station, not the main destination.

Step 2: The “Clean Sweep”

Identify all those “satellite” savings accounts you have scattered across different banks. Move the balances into your central Flourish Cash (or equivalent) account. Once the transfers are complete, you can close those old accounts, effectively deleting the “password fatigue” and the multiple tax forms that come with them.

Step 3: Map Your Mental Accounts

Now for the fun part. Inside Flourish, go to the Buckets tab and recreate your goals.

- Name your “Emergency Fund”

- Label your “Summer 2026 Italy Trip”

- Set aside a “Quarterly Tax” bucket

- Create a “New Car” fund

As soon as you drag and drop your total balance into these categories, your “mental accounting” brain will feel the same sense of organization it had before—only now, you’re viewing it all on one screen.

Step 4: Automate the Future

One of the most powerful features of this transition is the Automated Allocation tool. Instead of manually moving $100 here and $50 there every payday, you can set a rule: “Every dollar I send to Flourish should be split: 50% to General Savings, 30% to Taxes, and 20% to Vacation.” This turns your savings strategy into a hands-off system that runs in the background.

Safety in Numbers: Addressing the “Eggs in One Basket” Concern

One common reason people maintain multiple bank accounts is the fear of outgrowing the Federal Deposit Insurance Corporation (FDIC) limits. If you have substantial cash on hand—anything more than $250,000—manual bank-hopping used to be a necessity to ensure your savings were fully protected.

But here is where modern financial technology has changed the game. While it may look like you are putting all your eggs in one “Flourish basket,” the reality is quite the opposite.

The Power of the Program Bank Network

Flourish isn’t actually a bank; think of it as a high-tech “traffic controller” for your cash. It sits on top of a Program Bank Network that currently includes dozens of FDIC-member institutions—including well-known names like PNC, HSBC, and BNY.

When you deposit funds into Flourish, their algorithm automatically “sweeps” that money into these different banks. It ensures that no single bank in the network ever holds more than $250,000 of your money.

The Math of Massive Protection

By spreading your deposits across this vast network, Flourish is able to offer insurance limits that dwarf a traditional savings account. As of 2026, the limits are:

- Individual Accounts: Up to $7,500,000 in FDIC insurance.

- Joint Accounts: Up to $15,000,000 in FDIC insurance.

- Two-Person Households: Up to $30,000,000 in FDIC insurance.

To put that in perspective, to get $7.5 million of insurance the “old way,” you would have to manage 30 different bank logins. With Flourish, you get 30x the protection with a single password.

Technical Note #1 – the $30M Household Limit: This maximum coverage is achieved through “Account Categorization.” In a two-person household, this is typically reached by having two individual accounts (insured up to $7.5M each) and one joint account (insured up to $15M), all managed under the same household umbrella.

Technical Note #2 – The “Opt-Out” Feature: Many of our clients already have a mortgage or a local savings account with a big bank like PNC or Citibank. If you already have $250,000 at one of those banks, you don’t want Flourish to send more money there. You can simply “opt-out” of specific banks in the Flourish dashboard, and the algorithm will skip them, ensuring you never accidentally exceed the insurance limit at a bank you already use.

Conclusion: Simplification as a Financial Strategy

Perhaps the main message here is that financial peace of mind doesn’t always have to come with a side of complexity.

If you have multiple bank accounts and you’ve already developed good habits and systems for using them, you may not need to do anything. But if you’re seeking simplicity and possibly a better interest rate than what your banks are providing, consider whether consolidation makes sense, particularly if you can get into a “bucket-aware” platform like Flourish.

By creating digital buckets, you are giving yourself a way to satisfy the brain’s need for categorization without the inefficiency of “Narrow Bracketing” caused by having money scattered across different banks. It allows you to maintain the “psychological safety” of labeled funds while keeping the “economic reality” of a single, high-yield pool of capital.

If you have comments or questions on this piece, please drop me a line at: [email protected]

References

The information on this site is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Krishna Wealth Planning LLC (referred to as “KWP”) disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.

KWP does not warrant that the information will be free from error. None of the information provided on this website is intended as investment, tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall KWP be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the materials in this site, even if KWP or a KWP authorized representative has been advised of the possibility of such damages.

In no event shall KWP have any liability to you for damages, losses, and causes of action for accessing this site. Information on this website should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.