7-Minute Read

Happy New Year! As the calendar turns to January 1, 2026, many of us are focused on personal resolutions—health, travel, or perhaps more time with family. But for those in their 50s and 60s, the IRS has introduced a set of “financial resolutions” that may change how you save money.

In the last couple of months, you may have received a flurry of notices from your HR department or plan administrator. They were likely warnings about “Section 603” or “Mandatory Roth Catch-ups.” If you’re currently working, over age 50 (or turning 50 this year), and have access to a retirement plan at work, these changes aren’t just technicalities—they are the new foundation of your retirement strategy.

401(k) plans are often the primary retirement savings vehicle for our clients, and they remain a high priority in the savings policies we develop for them. This is largely because of the convenience of automatic paycheck deductions, but also because of the powerful compounding effect of tax advantages and employer matching contributions.

To help you hit the ground running this year, we’re diving into the mechanics of these changes. Here’s what we’ll cover today:

- How much can you contribute now? (Breaking down the new 2026 tiers).

- Are you affected by the mandatory Roth rule? (Checking your ‘Box 3’ wages).

- What if you have multiple jobs? (Navigating the aggregate limits).

- How do you turn this rule into a tax benefit? (The strategy behind the mandate).

- Where else should you be saving? (Coordinating with spousal plans and HSAs).

- How do you get the money out tax-free? (Managing your ‘buckets’ in retirement).

1. The 2026 Contribution Landscape: Three Tiers of Savings

Understanding your contribution limits is usually straightforward, but the SECURE 2.0 Act has introduced several nuances for 2026. While I frequently refer to the “401(k)” plan, these points generally apply to other similar retirement plans, such as 403(b), 457(b), and the federal Thrift Savings Plan (TSP). It is important to note that while the limits are similar, 403(b) and 457(b) plans have unique “lifetime” catch-up rules that we won’t cover here, but which may allow for even higher savings in specific scenarios.

Tier 1: The Base Limit (Under Age 50)

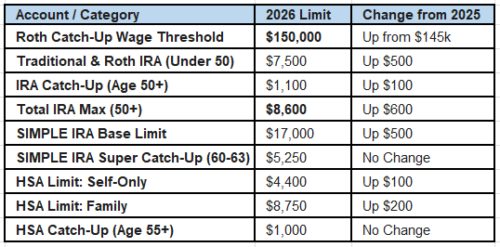

If you are under 50, you can contribute up to $24,500 to your 401(k) plan this year. This is a $1,000 increase over the 2025 limit, reflecting the IRS’s latest cost-of-living adjustments.

Tier 2: The Standard Catch-Up (Ages 50–59 & 64+)

Once you turn 50—or if you turn 50 at any point during the 2026 calendar year—you unlock the ability to “catch up.” For 2026, the additional amount is $8,000. This brings your total contribution potential to $32,500.

Tier 3: The “Super Catch-Up” (Ages 60–63)

This is the “Sweet Spot” created by the SECURE 2.0 Act. If you turn 60, 61, 62, or 63 this year, you are eligible for an enhanced catch-up contribution of $11,250. This brings your total annual contribution potential to an impressive $35,750.

The Age 64 “Cliff”: It is a common misconception that once you reach the higher limit, you stay there. However, the year you turn 64, your “Super” eligibility expires, and you revert to the Tier 2 standard catch-up. This makes the 60–63 window a critical “four-year sprint” for those looking to maximize their tax-advantaged growth just before retirement.

2. The “Forced Roth” Mandate: A New Reality for High Earners

Now, let’s address the headline change: Mandatory Roth Catch-ups. The new rule is simple on the surface but complex in execution: If you are eligible for catch-up contributions (age 50 or older) AND you had wages exceeding $150,000 in 2025, you are required to treat your catch-up contributions as Roth this year.

This mandate created significant challenges for 401(k) administrators over the last two years. They had to build new reporting logic into their systems to track prior-year wages and “force” a Roth designation on specific dollars. After a long transition period, those systems are now “live” as of today.

Identifying the $150,000 Threshold

The IRS uses a specific definition of income for this rule: FICA wages. This is the amount you earned from the sponsoring employer in the previous calendar year.

[Pro-Tip Box] When your 2025 Form W-2 arrives this month, look specifically at Box 3 (Social Security wages). This is the number that determines your status. If that number is $150,001 or higher, your catch-up contributions must be Roth.

Can’t wait for the W-2? Look at your final pay stub from 2025. Review your gross income—including salary and bonuses—but do not deduct your pre-tax 401(k) contributions. Because 401(k) deferrals do not reduce your Social Security wages, they are included in the $150k calculation.

Exceptions to the Mandate

- The “New Job” Exemption: If you started a new job with a new company on January 1st, 2026, you technically had $0 in wages from this specific employer in 2025. You are exempt from the Roth mandate for 2026, even if you earned $1M at your previous firm.

- Non-Aggregated Income: If you work two jobs and earned $100k at each, you are exempt. The $150k threshold applies per employer, not in aggregate across all your sources of earnings.

- Self-Employed Individuals: If you receive K-1 income or are a partner in a partnership, you do not have “W-2 wages.” Current guidance indicates these individuals are exempt from the “forced Roth” rule, allowing them to continue making pre-tax catch-ups in their Solo 401(k) or partnership plans.

3. Coordination and Caveats: The Fine Print

As you plan your 2026 savings, remember that you previously had a choice of making your catch-up contributions pre-tax or Roth. While that choice is now gone for high earners, you still have to manage the “logistics” of multiple accounts.

The “Double Max” Trap

If you have multiple jobs, each offering a retirement plan, you must comply with these contribution amounts in aggregate. You cannot “double max out.” If you turn 61 and have two jobs, your total employee deferral across both plans cannot exceed $35,750. Over-contributing creates a “distribution of excess deferral” nightmare that involves corrected W-2s and potential penalties if not caught by April 15th.

Administrator Adoption

I found that in many cases with clients last year, their plan administrators were not yet ready to allow the “Super Catch-up.” If your employer doesn’t offer a Roth 401(k) feature at all, the law is very strict: No one in that company is permitted to make catch-up contributions. The IRS is essentially using high earners’ desire for catch-ups as leverage to force employers to add Roth features to their plans.

4. Why This “Loss of Choice” is Actually a Strategic Win

Initially, being “forced” to pay taxes today feels like a loss of optionality. However, in many ways, this new rule can be incredibly beneficial. For years, many high earners have been prevented from making Roth IRA contributions because of their income levels. If a “Backdoor Roth IRA” wasn’t feasible because of existing Traditional IRA balances (the “Pro-Rata Rule”), they were stuck with pre-tax growth.

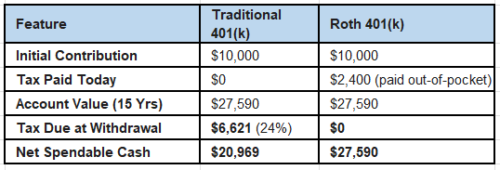

This is now a golden opportunity to build up your tax-free asset base. The graphic below assumes $10,000 grows at 7% annually over 15 years, with a current and future tax rate of 24%.

The downside is immediate: you will likely see less net take-home pay. Because your employer must withhold taxes on those catch-up dollars, your “net” check will decrease once you reach the $24,500 base limit and the “forced Roth” catch-ups begin. We call this “Tax Bracket Arbitrage.” You are paying the tax at today’s known rates to hedge against the risk that tax rates will be higher when you retire.

5. Beyond the 401(k): Expanding Your Strategy

Perhaps cash flow doesn’t allow you to reach the $35,750 maximum, or you prioritize other forms of savings. Here is how the new rules affect your broader strategy for accumulating wealth::

- Spousal Coordination: If you are married and your spouse earned under $150k, consider maximizing their 401(k) on a pre-tax basis first. This allows the household to still get a tax deduction while you fulfill your Roth mandate.

- The Health Savings Account (HSA) Advantage: For those focused on reducing taxable income, the HSA remains the “triple-tax-advantaged” unicorn. The 2026 limits are $4,400 (Self) and $8,750 (Family).

- Non-Qualified Deferred Compensation (NQDC): For executives, if the “forced Roth” rule makes your current tax bill too high, an NQDC plan may allow you to defer even larger amounts of salary and bonuses pre-tax, though these plans come with unique rules and risks.

- Roth IRAs: The 2026 limit is $7,500 (plus $1,100 for age 50+). Remember that you are phased out of direct contributions if your MAGI is over $168k (Single) or $252k (Joint).

6. The Finish Line: Accessing Your Wealth

When you retire with a 401(k) containing both pre-tax and Roth funds, you gain significant flexibility. But the rules for accessing that money depend heavily on how you structure your accounts.

Option A: Distribution from the Plan

Most plans will allow you to choose which “bucket” to pull from. You can request a distribution from only your Roth balance for tax-free cash, or only your pre-tax balance if you want to fill up a lower tax bracket.

- The 5-Year Rule: For Roth 401(k) earnings to be tax-free, you must be 59 ½, and the account must have been open for five years. Note that each 401(k) has its own “clock.”

Option B: The “Split Rollover”

To gain even more control, you can execute a direct rollover into separate IRAs:

- The Pre-tax balance (usually including all employer matching) goes into a Traditional IRA.

- The Roth balance goes into a Roth IRA.

In an IRA structure, you gain a massive benefit: First-In, First-Out (FIFO) rules. You can access your original Roth contributions at any time tax-free, even if the account hasn’t been open for five years. Only the earnings are subject to the 5-year clock.

Your 2026 Action Items

- Check Your Elections: Ensure you are on track to hit the new $32,500 or $35,750 max.

- Review Your Pay Stub: Watch for the shift to Roth once you exceed the base limit.

- Coordinate with your Advisor: Let’s look at your 2026 projections to ensure your “tax buckets” are balanced.

Happy New Year—here is to a prosperous and tax-efficient 2026!

If you have comments or questions on this piece, please drop me a line at: [email protected]

References

- https://www.irs.gov/pub/irs-pdf/fw2.pdf

- https://krishnawealth.com/cultivate-your-optionality/

- https://krishnawealth.com/do-we-underestimate-the-benefit-of-health-savings-accounts/

The information on this site is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Krishna Wealth Planning LLC (referred to as “KWP”) disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.

KWP does not warrant that the information will be free from error. None of the information provided on this website is intended as investment, tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall KWP be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the materials in this site, even if KWP or a KWP authorized representative has been advised of the possibility of such damages.

In no event shall KWP have any liability to you for damages, losses, and causes of action for accessing this site. Information on this website should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.