6-Minute Read

Most financial advice focuses on the accumulation or protection of money. This includes spreadsheets, compound interest tables, and “hacks” to save an extra 1% on our tax returns. I’ll admit I love all of that stuff. Back in my engineering days, the very first computer program I ever wrote for “fun” was a time-value-of-money calculator. But let’s acknowledge that little is said about the second, more difficult half of the equation: the utility of money.

In his book The Art of Spending Money, Morgan Housel suggests that spending money is a skill—one that is surprisingly difficult to master. While saving is mostly a math problem, spending is a psychological minefield. We assume that having more money will naturally lead to greater happiness, but without a system, we often find ourselves on a “hedonic treadmill,” running faster and spending more just to remain in the same emotional state.

If we want to get the most out of our money, we must stop treating spending like a reflex and consider treating it like an engineering challenge. By leveraging the Contrast Principle and a commitment to Experimentation, we can begin to “optimize” our joy. Let’s explore how in this short piece.

The Biology of the “Reset”: The Contrast Principle

The biggest enemy of happiness is habituation. Humans are remarkably good at getting used to things. The first time you stay in a five-star hotel, you feel like royalty. The twentieth time you do it, you’re just annoyed that the room service is five minutes late.

This is the Hedonic Treadmill in action. When luxury becomes your “baseline,” it ceases to provide pleasure; it simply becomes the new standard you must maintain to avoid feeling inadequate. To engineer happiness, you must maintain a low baseline. In dollar terms, this baseline level will depend on your specific financial circumstances. Just know this isn’t about deprivation or being guilted into frugality; it’s about protecting your ability to experience a “peak.”

The “Mango Season” Effect

At a biological level, your brain doesn’t actually crave “more”—it craves novelty and contrast.

Neuroscience explains this through a concept called Reward Prediction Error. Think of the first Alphonso mango of the season. Because you haven’t tasted that specific, sun-ripened sweetness for an entire year, that first bite is an explosion of flavor. Your reality vastly exceeds your “baseline” expectation of fruit, and your brain floods with dopamine as a result.

However, if you lived in a world where it was mango season every single day, by day 90, that same fruit wouldn’t be an event. It would just be breakfast. The “upward error” disappears because excellence has become your new normal.

By keeping your daily life simple—eating home-cooked meals, driving a modest car, or enjoying free hobbies—you are essentially resetting your dopamine receptors. You are protecting the “seasonality” of your joy. When you do decide to spend on a luxury experience, the contrast between your baseline and the event is so vast that the resulting happiness is significantly higher than if you lived in a permanent state of medium-high luxury.

Engineering your spending means realizing that the “daily mango” eventually tastes like nothing at all. Contrast is the key. Find it and protect it.

The Struggle of “Knowing”: Why We Fail at Spending

If spending for happiness were easy, we’d all be blissful. But as Housel points out, spending is a social and psychological minefield. I’ll be the first to admit: I personally struggle with this. If I’m not careful, I can find myself in a state where I’m not even anticipating happiness from spending money. It feels like a chore or a default setting. These words are as much for me as they are for you!

Why is it so hard to know what will make us happy?

- Social Mimicry: We often spend money on what society says is luxurious (flashy cars, expensive watches) rather than what actually resonates with our unique personalities.

- Affective Forecasting: Psychologists have found that humans are terrible at predicting how they will feel in the future. We think the new kitchen will change our lives; three months later, it’s just the place where we toast bread.

- Frugality Trauma: For those of us (like myself) who spent years in a “saving” mindset, spending can actually trigger anxiety rather than joy. We’ve optimized for “number go up” for so long that “number go down” feels like a failure.

The Subjectivity of the “Peak”

While the biology of the “Mango Effect” is universal, the “mango” itself is not.

For some, that high-contrast peak might be a $200 fountain pen that makes every hour of work feel like a creative act. For others, it might be the silence of a solo hiking trip or the vibrant chaos of a front-row seat at a sporting event.

An important reminder: where you derive pleasure from spending is entirely unique to you. No one—not a financial planner, not a book, and certainly not social media—can tell you how to spend your money to feel alive. We all have different “joy triggers.” I’m not here to hand you a template for a perfect life; I just want to bring a little more awareness to the expenditures that support your life.

Spending as Research: The Power of Experimentation

Since we are bad at predicting what will make us happy, we have to stop guessing and start experimenting. Think of your spending as a laboratory. As Housel writes, you aren’t “wasting” money; you are buying data points.

The Success of a “Failed” Purchase

One of the biggest hurdles to experimentation is the fear of waste. We’ve been conditioned to believe that every dollar spent must return a predictable unit of satisfaction. If we buy a high-end gadget and it gathers dust, we label it a “waste.”

But in the laboratory of spending, there is no such thing as a failed experiment.

If you spend money on something and realize it didn’t bring you joy, you haven’t lost that money—you’ve purchased the knowledge that you don’t need to spend on that category ever again. You have successfully narrowed down your personal “joy map.” When you realize that a five-star hotel doesn’t actually make you sleep better than a boutique guest house, you’ve just saved yourself thousands of dollars in future “default” spending.

Try a “Spending Sprint”

To find your peaks, try these low-stakes experiments:

- The Ultra-Premium Trial: Spend 10x your usual amount on one specific category (e.g., coffee, socks, or stationery) for a week. Does it feel 10x better? If not, your “cheap” version is a great value.

- The “Outsourcing” Experiment: Spend money to eliminate your least favorite task for a month (like cleaning, bookkeeping, or yard maintenance). Does the reclaimed time actually make you happier?

- The “Solo Spend”: Buy something that provides zero social status—something nobody else will ever see. This helps you decouple “joy” from “signaling.”

The Engineering of Flexibility: Fixed vs. Variable

I have a habit of connecting engineering principles to personal finance. It doesn’t always map cleanly, but one concept is “signal to noise”. From an engineering perspective, the most dangerous thing you can do to your joy “signal” is to increase your fixed costs. When you buy a massive house or an expensive car lease, you are raising your baseline permanently. You are locking yourself into a high-cost lifestyle that offers zero contrast because it becomes the background “noise” of your life.

The goal is to keep your fixed costs low and your variable costs high. This creates a “shock absorber” for your happiness. When your mortgage and car payments are modest, you have the financial margin to engage in the spending sprints I mentioned earlier. You can afford the high-contrast peaks because you haven’t drowned your budget in a sea of recurring, invisible luxuries that you’ve long since stopped noticing.

As Housel notes, the best thing money can buy is “the ability to do what you want, when you want,” and that requires a lean engine.

Conclusion: Designing Your Personal “Joy Map”

We started with essentially this question: Can happiness be optimized or engineered based on the way you spend money?

The answer is yes, but not through the pursuit of a permanent state of luxury. True optimization comes from the rhythmic movement between a simple, disciplined baseline and the occasional, high-contrast peak. It comes from the willingness to try new things and the awareness to admit when an experiment didn’t work.

Remember, the “Mango Effect” only works if there is a season when the mangoes are gone. If you live at the ceiling of your means, your life becomes a flat line of “medium-high” satisfaction that eventually feels like nothing at all.

I’m not here to tell you to be a minimalist, nor am I admonishing you for being a spendthrift. I’m here to suggest that you bring a scientist’s curiosity to your wallet. Keep your fixed costs low, keep your eyes open for what truly makes your heart beat a little faster, and don’t be afraid to buy a few “wrong” things on your way to finding the right ones.

Money is a tool for freedom, but the art of spending that money is using that freedom to find the contrast that makes life feel vivid.

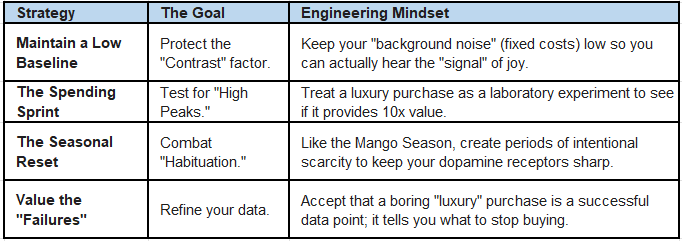

The Joy Map: A Quick Reference Guide

If you have comments or questions on this piece, please drop me a line at: [email protected]

References

- https://www.goodreads.com/book/show/231148075-the-art-of-spending-money

- https://krishnawealth.com/is-a-dose-of-minimalism-the-cure/

The information on this site is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Krishna Wealth Planning LLC (referred to as “KWP”) disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.

KWP does not warrant that the information will be free from error. None of the information provided on this website is intended as investment, tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall KWP be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the materials in this site, even if KWP or a KWP authorized representative has been advised of the possibility of such damages.

In no event shall KWP have any liability to you for damages, losses, and causes of action for accessing this site. Information on this website should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.