5-Minute Read

At the time of this writing, conventional mortgage rates across the country are below 3 percent as they have been for several months during the global pandemic. Perhaps you’ve already taken some action to refinance. If not, how should you think about this decision?

The goal of this piece is three-fold. First, we’ll explore several questions you should answer before refinancing your mortgage. We’ll then briefly look at an example to show the potential costs savings of refinancing. Finally, we’ll provide an alternative to traditional refinancing if you are nearing retirement.

Considerations for Refinancing your Home Mortgage

There is always some element of risk to a refinancing decision. One common concern is if interest rates go down further after you’re locked in a new loan. In today’s low interest environment, higher future interest rates would seem to be the more noteworthy risk to mitigate. Here are some “checklist” questions to ask to gauge how appropriate a refinance would be for your household.

Do you plan to live in the same house for at least a few years?

If the answer is no, there’s a good chance the costs (both in dollars and time) may not exceed the benefits of refinancing. It is fairly straightforward to calculate how much time it will take to “breakeven” from refinancing. The middle section of this piece touches on this a little.

Is your “loan to value” less than 80 percent?

Take your current mortgage balance and divide it by your estimate of the fair market value of your home. If that ratio is more than 80 percent, it may be more difficult to refinance. You might also be subject to private mortgage insurance.

Has your credit score recently improved?

This isn’t necessarily a requirement. But if the answer is yes, it improves your odds of qualifying for a lower interest rate on a mortgage.

Do you have other debts with higher interest rates?

If the answer is yes to this (and the previous two questions), then you might consider getting cash out as part of the refinance. This may help give you some breathing room with servicing your other debts. But if your situation or behavior results in getting back to that previous state of indebtedness, refinancing may not be much more than a temporary band aid.

Notably, cash from a refinance doesn’t have to be used to pay off other debts. In some cases, based on your circumstances and risk tolerance, the cash can be used to invest which can turn out to be a productive use of capital in the long run.

Is your goal to lower the overall interest paid?

If yes, then consider a shorter-term mortgage (e.g. 15 years with a fixed rate). You can also make additional principal payments, either periodically or systematically. This helps you pay off the debt faster and reduce your interest costs. If this were your goal, you probably would want to avoid or minimize the amount of cash taken out during the refinance.

Is your goal to reduce your monthly mortgage payment?

If yes, then consider a longer-term mortgage (e.g. 30 years with a fixed rate). Financial discipline is important in this case. If you can generate cash flow savings from a refinance, then where can you apply that savings to make a real difference? A few suggestions:

- If you have younger children, can you start or increase contributions to a 529 college savings plan?

- Can you further maximize your tax-free assets?

- Can you increase retirement savings to boost your “retirement number”?

Are you refinancing after December 1st, 2020?

One headwind you’ll face if you’re refinancing on or after this date is that Fannie Mae and Freddie Mac are implementing a 50-basis point (0.50%) “adverse market refinance fee” to shore up risk exposures. If this applies to you, this will need to factor into your decision.

Potential Cost Savings of Refinancing

To briefly show “why” refinancing can be attractive, consider the following scenario:

- Assume you acquired a home six years ago with a $300,000 mortgage.

- The mortgage had a 30-year term with a fixed interest rate of 4.0%.

- Until now, you paid only the required payment of $1,432 per month (excluding property taxes and home insurance). As a result, your current mortgage balance is now approximately $264,000 today.

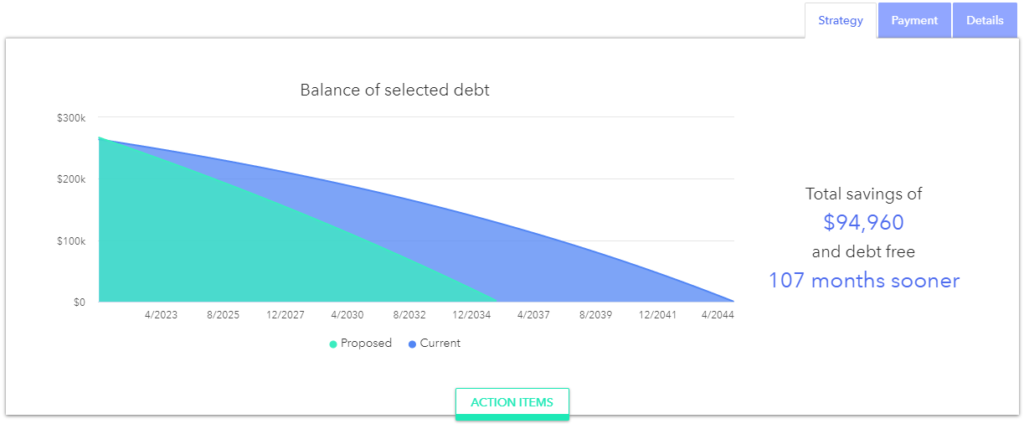

If your goal were to lower your overall interest paid, you could consider refinancing to a new mortgage with a 15-year term and fixed interest rate of 2.4%. If you rolled in $3,000 in total closing costs, your new mortgage would be $267,000. This also assumes no cash out. Your monthly payment would increase from $1,432 to $1,768. But as the picture below (courtesy of RightCapital) shows, you would pay off the debt almost 9 years sooner and save a little under $95,000 in total interest costs.

Notably with the interest rate differential in this example, you would breakeven from the refinancing costs in under one year. Of course, not all refinancing situations will be as attractive as this. It is just a framework for thinking about the decision and illustrating the potential benefits.

An Alternative Refinancing Approach if You’re Near Retirement

Generally, if you’re nearing retirement and have an existing mortgage, you may have an additional incentive to refinance. That is because you’re still working and have reportable income that can help with qualifying for a loan with an attractive rate. There may be limitations if you wait to refinance after retirement.

That said, you might also consider an alternative to a “traditional” mortgage refinance. If you’re at least age 62, look at the HECM reverse mortgage.

While we don’t have the space to cover all the nuts and bolts here, the main reason to consider this approach is for the flexibility. With a traditional mortgage, you are required to make payments month in and month out. If you don’t, you risk foreclosure.

With a reverse mortgage, you can choose to pay it down monthly just like a traditional mortgage, but you have the choice. This optionality can help if emergencies arise or we enter a downturn in the markets, and you don’t want to liquidate assets during that time.

There a several other ways to think of a reverse mortgage strategically. I noted several of those in a piece a few years ago: 5 Ways a Reverse Mortgage Can Help Your Retirement

Reverse mortgages do have higher upfront costs and other considerations to carefully review before moving forward.

If you have comments or questions on this piece, please drop me a line at: [email protected]

References

- https://www.consumerfinance.gov/ask-cfpb/what-is-private-mortgage-insurance-en-122/

- https://krishnawealth.com/enhancing-your-college-savings-529-plan-experience/

- https://krishnawealth.com/seven-ways-to-maximize-your-tax-free-assets/

- https://krishnawealth.com/two-ways-of-quantifying-your-retirement-readiness/

- https://www.housingwire.com/articles/the-adverse-market-fee-the-gses-added-to-refinance-loans-is-unwarranted/

- https://www.hud.gov/program_offices/housing/sfh/hecm/hecmhome

- https://www.nextavenue.org/5-ways-a-reverse-mortgage-can-help-your-retirement/

The information on this site is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Krishna Wealth Planning LLC (referred to as “KWP”) disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.

KWP does not warrant that the information will be free from error. None of the information provided on this website is intended as investment, tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall KWP be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the materials in this site, even if KWP or a KWP authorized representative has been advised of the possibility of such damages.

In no event shall KWP have any liability to you for damages, losses, and causes of action for accessing this site. Information on this website should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.